Whose Data Is Your Agent Running On?

The quiet question that's about to decide who wins in financial AI.

Apologies for the radio silence last couple weeks- I was busy watching the market cross a line it had spent the last year debating.

Agents are no longer theoretical. They’re live, and that has changed the real question entirely.

Six months ago, the hard question in financial AI was whether an agent could be trusted to act - to move money, place a trade, file a report - without a human pressing the button each time. We spent the better part of a year debating autonomy.

That debate is mostly settled now. Agents act. They’re acting in production, at institutions you’d recognise, in workflows that used to be untouchable.

So the question moved. And it moved somewhere more interesting - and more uncomfortable.

Because an agent that can act is only as good as what it knows. Point a brilliant model at thin, generic, or badly-governed data and you get confident nonsense at machine speed. Point that same model at deep, proprietary, well-grounded data and you get something that starts to look like genuine institutional judgement. The model, it turns out, was never the moat. The intelligence beneath it is.

That realisation is quietly rearranging the entire industry. Everyone is now racing to own the layer the agents run on - the data, the analytics, the grounded reasoning that makes an AI output something you’d actually stake a decision on. It’s a quieter fight than the one about autonomy. It doesn’t make for dramatic demos. But it’s the one that will decide who wins.

And it has a sharp edge most people haven’t fully realised yet: if intelligence is the asset, then control over access to that intelligence is power. The institution that grounds its agents in something nobody else has is building a moat. The institution that builds everything on an intelligence layer it doesn’t own is building on someone else’s terms - and this month, more than one of them found out exactly what that means.

Let’s get into it.

- The Editor

THE BRIEF - Four Things Worth Knowing

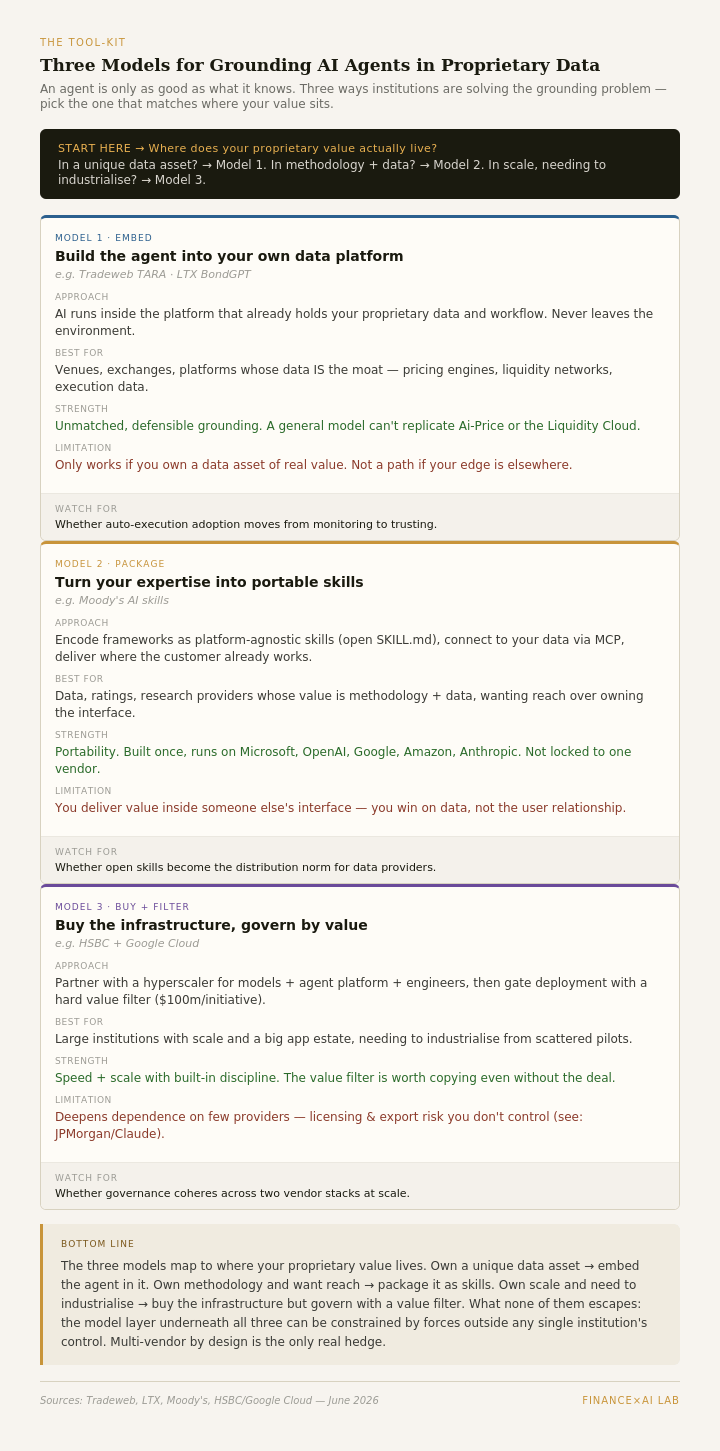

HSBC put a $100 million price tag on every AI project. That filter matters more than the deal

HSBC and Google Cloud announced a multi-year partnership, targeting more than 200 new AI use cases over two years - built on Gemini models, the Gemini Enterprise Agent Platform, and an existing base of 600+ HSBC applications already running on Google Cloud. The three opening focus areas are familiar: wealth management support, financial crime risk management, and frontline tools for relationship managers.

But the headline number isn’t the 200 use cases. It’s the filter HSBC is applying to them. Only initiatives the bank estimates could each return more than $100 million - in direct revenue or efficiency - get prioritised for delivery. That single sentence is the most useful thing in the announcement.

Here’s why it’s worth your attention regardless of whether you’ll ever sign a hyperscaler deal. Most institutions are still struggling with AI prioritisation as a qualitative exercise - which projects feel promising, which sponsors are loudest, which use cases demo well. HSBC has replaced that with a value gate: articulate the return before you invest, or it doesn’t make the list. It’s the difference between an AI strategy and an AI wish list. The financial-crime detail makes it concrete - HSBC monitors nearly a billion transactions a month and expects to intervene twice as fast under the new architecture, which is a measurable target, not an aspiration.

The takeaway: Steal the filter, not the vendor. Before your next AI initiative, ask the HSBC question - what’s the quantified return, and over what horizon? If the project can’t survive that question, it shouldn’t survive your roadmap.

One honest caveat: a $100m estimate set by the institution investing in it is a prioritisation gate, not a realised result. Treat it as a planning discipline, not a track record.

Tradeweb and LTX made the same bet 24 hours apart: the data is the moat, not the model

Within a day of each other, two credit-trading platforms shipped AI that tells you exactly where fixed-income markets are heading - and they did it from opposite ends of the same idea.

Tradeweb launched TARA, a conversational assistant embedded in its institutional platform for US credit. Traders ask, in plain language, about trading activity, market flows, execution performance, liquidity and pricing - and TARA answers from Tradeweb’s proprietary historical and intraday data, plus its Ai-Price pricing engine. T. Rowe Price is an early adopter. The point isn’t the chat interface. It’s that the answers are grounded in data no competitor can replicate.

LTX, backed by Broadridge, launched agentic capabilities in BondGPT - the more aggressive move. Traders now build agents that monitor live market conditions and take action: generate alerts, create trade tickets, select dealers, launch RFQs, and accept prices to auto-execute. All under trader-defined parameters, with human-in-the-loop approvals, explainability before every action, and full auditability. Goldman, J.P. Morgan, Morgan Stanley, BofA and TD recently joined as integrated liquidity providers.

Put them side by side and you can see the whole direction of credit-market AI. Tradeweb proves the grounding thesis: the model is a commodity, the proprietary data is the defensible asset. LTX proves the autonomy thesis: AI is crossing from “answer my question” to “execute my trade.” Both are true at once, and both run on data the platform owns.

The takeaway: If you’re evaluating any AI trading or analytics tool, the sharpest question isn’t “how good is the model?” - models converge fast. It’s “what data is it grounded in, and can a competitor get the same?” That’s where durable advantage actually lives. And on the autonomy side, watch LTX’s own framing: auto-execution is live, but they expect traders to monitor before they trust. The binding constraint on agentic execution isn’t the technology. It’s how fast a desk is willing to let go of the button.

Moody’s turned 115 years of credit analysis into something any AI platform can call

Moody’s launched its first set of AI “skills” - and this one rewards a close read, because it’s the cleanest expression of where data providers are heading.

A skill is a packaged instruction kit that encodes Moody’s analytical frameworks and connects an AI agent to its proprietary ratings, research and risk intelligence. The first five cover real analyst workflows: earnings-call summaries, peer analysis, public information books, rating pitches, and sector analysis. They launch on Microsoft 365 Copilot Cowork first, but here’s the crucial part - they’re built on the open SKILL.md standard, which means the same skill runs on any compatible platform: Microsoft, OpenAI, Google, Amazon, Anthropic.

Think about what that actually does. Moody’s isn’t selling you a model, and it isn’t building a walled-garden app. It’s packaging its methodology and its proprietary data into a portable asset that travels to wherever you already work - and because the standard is open, that institutional knowledge isn’t locked to any one AI vendor. The strategic repositioning underneath is the real story: data providers are moving from “we have the data” to “we have the grounded reasoning that makes anyone’s AI output valid, explainable, and auditable.” Moody’s has already signalled credit analysis, due diligence, and insurance underwriting are next.

The takeaway: This is a preview of how specialised financial expertise gets distributed in an agentic world - not as a subscription you log into, but as skills that plug into your existing AI stack. If you’re a data or analytics provider, the question is whether you’re building skills or still building apps. If you’re a buyer, the question is whether your AI tooling can consume grounded skills from providers like Moody’s - because that’s about to become the difference between an agent that guesses and an agent that cites.

JPMorgan cut off Claude in Hong Kong- The reason wasn’t performance, and that’s the lesson

Every story above is about building on AI. This one is about what happens when the ground underneath shifts without warning.

JPMorgan stopped its Hong Kong staff from accessing Anthropic’s Claude models. The trigger wasn’t model quality or cost. It was contractual - the wording of Anthropic’s licensing terms, which exclude usage across Greater China including Hong Kong. JPMorgan simply removed Claude from the internal list of approved models for that region. Goldman Sachs made the identical move in April. The backdrop: days earlier, on June 13, Anthropic had suspended its frontier Mythos and Fable models worldwide for all foreign nationals after a US export-control directive.

For a practitioner, this is the most important story in the issue, even though it ships no product. Everything else here assumes the intelligence layer is stable - that the model you build your agent on today is the model you’ll have tomorrow. This is the reminder that it might not be. When your AI capability depends on a US frontier-model provider, access can be revoked by geography, by a licensing clause, or by an export directive - none of which you control, and any of which can land overnight. There’s a quiet irony worth noting: several of the banks restricting Claude regionally are reportedly lined up to lead Anthropic’s IPO. They’re underwriting the company and ring-fencing it at the same time.

The takeaway: Treat model access as a supply-chain risk, not a settled utility. The practical move is the one HSBC is already making - multi-vendor by design (Google and Mistral), so no single provider’s licensing terms or a government’s export policy can take a critical capability offline. If your AI roadmap has a single point of failure at the model layer, this month is your warning to build the hedge before you need it.

The Workflow

How an AI Agent Executes a Bond Trade - From Market Signal to Settled Trade

Use case: agentic fixed-income trading (the LTX BondGPT model). Applicable to: buy-side trading desks, portfolio managers, and execution teams in corporate credit - and, increasingly, rates.

Corporate bond markets are fragmented and opaque. A trader watching for a specific condition - a bond hitting a target spread, a liquidity window opening - has to monitor continuously, then manually move through discovery, dealer selection, RFQ, and execution. By the time that chain completes, the opportunity is often gone.

An agentic trading workflow compresses that chain. But it’s worth being precise about how it differs from the agentic workflows we’ve covered before. An AML agent assembles evidence and hands it to a human to judge. A trading agent can be authorised to act. That single difference is why the entire architecture here is built around bounded authority and explainability - because when an agent can spend money, the guardrails aren’t a feature, they’re the product.

Walk through the diagram and the design logic becomes clear. The mandate comes first, and it’s human - the trader defines, in plain language, what condition to watch, what to do when it fires, and the hard limits on size and scope. Everything the agent does downstream is constrained by what’s set at this step. Then the agent takes over the part humans are worst at: continuous monitoring across a fragmented market, all day, without fatigue.

The pivot point is step three. When a condition fires, explainability is mandatory before any action. For a low-authority mandate, the agent stops and hands to the human. For a higher-authority one, it proceeds - but only after showing its reasoning, so the trader can see why it’s about to act, not just that it acted. From there the agent handles dealer selection and the RFQ - and this is where the proprietary-data moat from The Brief shows up in practice: intelligent counterparty selection only works if there’s deep, reachable liquidity in the network to act against.

Step five is the consequential one. If the returned price meets the trader’s parameters, the agent can accept it and auto-execute. This is the genuine “analysis to action” moment - live on the platform today, and the capability institutions will adopt most cautiously. Every step, finally, lands in a full audit trail: what fired, what the agent did, what price it took, against what limits. That’s what post-trade compliance and model-risk teams examine, and it’s built in rather than bolted on.

The problem that hasn’t been solved is trust velocity. The architecture works and auto-execution is live, but the binding constraint isn’t technical - it’s behavioural. How quickly will a buy-side desk move from monitoring the agent to trusting it to trade unsupervised? There’s also no public, third-party validation yet of latency, execution quality, or audit artifacts versus a human workflow. Until that exists, the highest-autonomy mode stays slow to adopt - and that caution is the correct instinct, not a failure of the technology.

The takeaway: If you’re assessing an agentic execution tool, don’t start with the model. Start by mapping exactly where the human authority boundary sits - step 1 (mandate), step 3 (explainability gate), and step 5 (execution). The quality of a trading agent isn’t in how much it can do autonomously; it’s in how precisely you can bound what it does, and how clearly it shows its work before it acts. A tool that makes those boundaries crisp is safer than a more capable one that blurs them.

The Toolkit

Weekly Coverage - The Broader Signal

Lloyds - The Readiness Number

Lloyds’ sentiment survey is the clean industry-pulse datapoint: 93% say AI/ML will have the biggest impact on UK financial services over the next five years, 91% expect AI investment to rise in the next 12 months, 77% call emerging-tech investment a growth priority. Backing it with action - 300 new tech hires for AI (per the Guardian), and £50m of AI value delivered in 2025 with £100m+ expected in 2026.

The signal: intent and budget are no longer the bottleneck. Grounding and execution are.

Broadridge + Anthropic, Project Glasswing - AI spend moves into defence

Broadridge joined Anthropic’s Project Glasswing, applying the unreleased Claude Mythos Preview model to harden cyber defences across critical financial software.

Use case: defensive security on infrastructure that underpins $15 trillion in average daily trading.

Why it matters is because it shows AI budget in finance flowing somewhere other than productivity and revenue - into cyber resilience.

THE IRONY

This is the same Mythos-class model family pulled from foreign-national access under the US export directive days earlier. The defensive capability and the national-security risk are two faces of the same model.

UK Finance Fraud Report - the intelligence layer cuts both ways

The Annual Fraud Report is the sobering counter-signal to every build story this month: £1.28 billion stolen through payment fraud in 2025 (up 4%); APP fraud at £576.4m (up 19%); investment fraud the single biggest category at £221.5m, up 40% year-over-year. Two-thirds of APP fraud starts online. Criminals are industrialising with deepfakes, cloned voices, and synthetic identities at scale.

The same grounding-in-data that powers a trading desk powers a scam. The report’s core argument lands on the platforms where the fraud originates: banks can’t be the only line of defence.

Mastercard Agent Pay for Machines - the payments edition of the governance problem

Mastercard launched infrastructure for machine-to-machine payments: credentialing, programmatic spend limits, and guaranteed multi-rail settlement across cards, accounts and stablecoins, down to fractions-of-a-cent microtransactions. 30+ partners including Stripe, Adyen, Coinbase, Ripple, Solana Foundation.

Use case: autonomous agents transacting with each other at machine speed.

The thread to this issue: as agents act, the payment rail needs its own trust layer - credentialed identity, enforced limits, full auditability. Same governance challenge, money-movement edition.

Experian Agent Operating System - the grounding problem, stated as a survey

Experian launched its Agent Operating System (June 2, Money20/20 Europe) within the Ascend Platform - a governed layer bringing Experian, client, and partner agents together for data, decisioning and control across the lending lifecycle (ServiceNow as first integration partner).

Use case: scaling agentic AI across the lending lifecycle without losing governance.

The datapoint that fits the theme: 48% of organisations say integrating data into AI workflows is the hard part; a third cite poor data lineage; a third cite siloed data. That is the intelligence-layer problem, in the industry’s own words - and it’s why this issue is named for it.

One question Before You Go

Everything in this issue points the same direction: the skill that mattered most five years ago - knowing how to do the analysis, is quietly being replaced by knowing how to direct, ground, and check an agent that does it for you.

One click. No follow-up unless you want one. We’re trying to understand where our readers actually are.

Everything here is built around one question: does it make adapting easier for you? The case studies, the worked examples, the expert conversations - that’s the whole point. I just wrapped one last week, and there’s an exciting one to announce soon.

See you soon!

Have a good rest of the week everybody.

Thanks,

Swati Sharma

Editor-in-Chief

Finance×AI Lab